Travel restrictions, and the cancellation of many planned visits, flights, business and leisure events due to COVID-19 are already severely affecting many service sectors and this is likely to persist for some time, underscored today the OECD in their Interim Economic Assessment publised today.

The cut in outbound tourism from China would affect Japan, Korea and some other smaller Asian economies the hardest, but the risk of a drastic and widespread reduction on foreign visitors arrivals pushing down growth in major economies in the OECD is on the rise as tourism contributes a 4.25% of global GDP and a 7% of total job creation as a whole in OECD economies.

One-thenth of all cross border visitors come from China

Worldwide, Chinese tourists account for around one-tenth of all cross-border visitors, and one-quarter or more of all visitors in Japan, Korea and some smaller Asian economies (Figure 4, Panel A).

Exports of travel services to China, including the spending by Chinese visitors, are also high in many countries.

Cease in outbound tourism from China represents a sizeable near-term adverse demand shock. This is already apparent in many destinations; visitor arrivals in Hong Kong, China in February were 95% lower than usual.

International arrivals widespread cut, around the corner

If the spread of the coronavirus outbreak affects visitor numbers more widely across the major economies, there would be sizeable costs, with tourism accounting directly for 4¼ per cent of GDP in the OECD economies and almost 7% of employment.

Risk of recession including Japan and the Eurozone in case of broader contagion

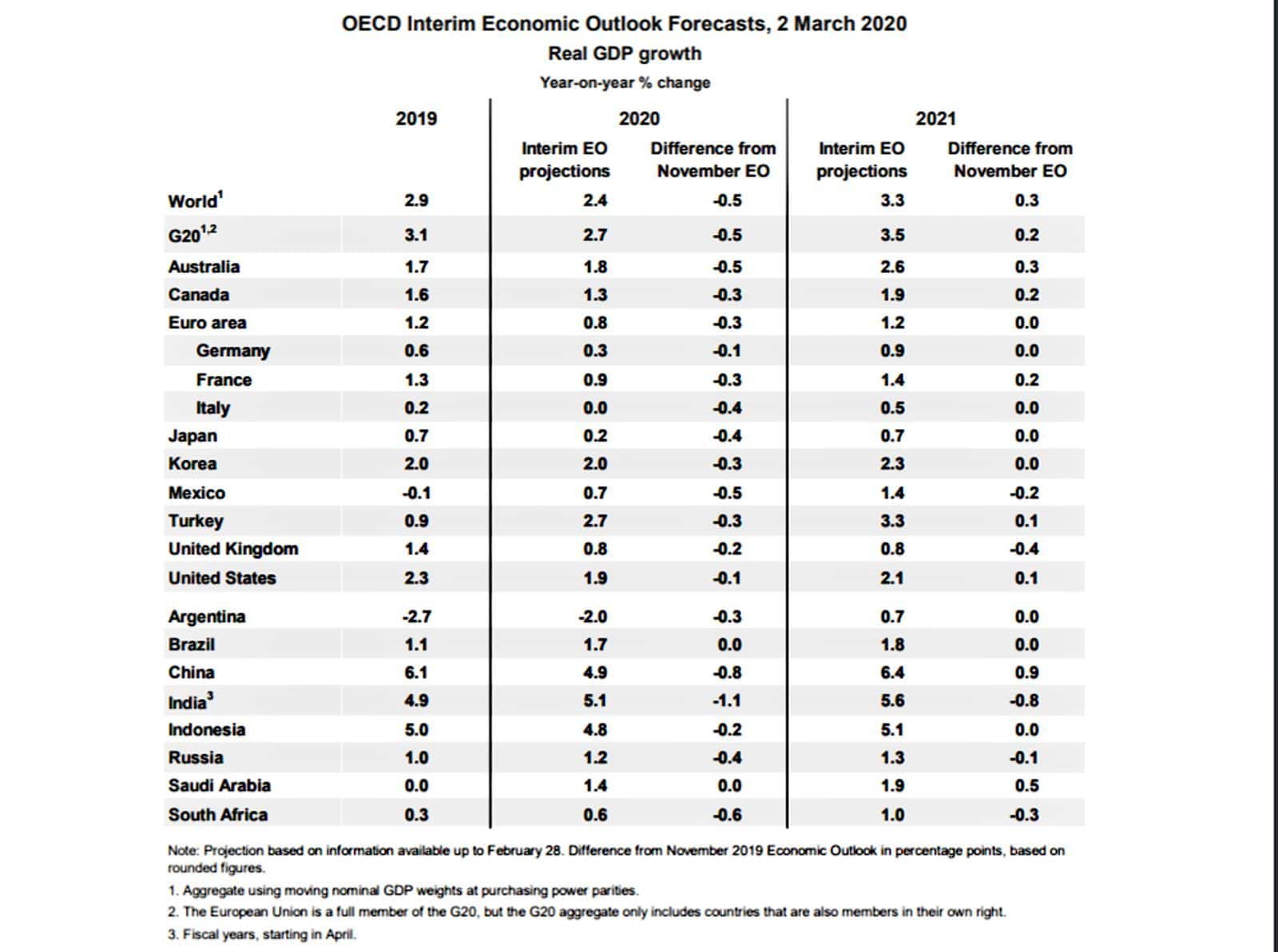

Even in the best-case scenario of limited outbreaks in countries outside China, a sharp slowdown in world growth is expected in the first half of 2020 as supply chains and commodities are hit, tourism drops and confidence falters. Global economic growth is seen falling to 2.4% for the whole year, compared to an already weak 2.9 % in 2019. It is then expected to rise to a modest 3.3% in 2021.

Growth prospects for China have been revised down sharply to below 5% this year after 6.1% in 2019.

Presenting the Interim Outlook in Paris today, OECD Chief Economist Laurence Boone said: “The virus risks giving a further blow to a global economy that was already weakened by trade and political tensions. Governments need to act immediately to contain the epidemic, support the health care system, protect people, shore up demand and provide a financial lifeline to households and businesses that are most affected.”

OECD warns that all their projections assume the end of the commercial tensions between the USA and China and that the European Union and the UK reach a commercial agreement for Brexit in time.

A) The worst scenario: broader contagion not contained:

Broader contagion across the wider Asia-Pacific region and advanced economies, as has happened in China, could cut global growth to as low as 1.5% this year, halving the OECD’s previous 2020 projection from last November. Containment measures and loss of confidence would hit production and spending and drive some countries into recession, including Japan and the euro area.

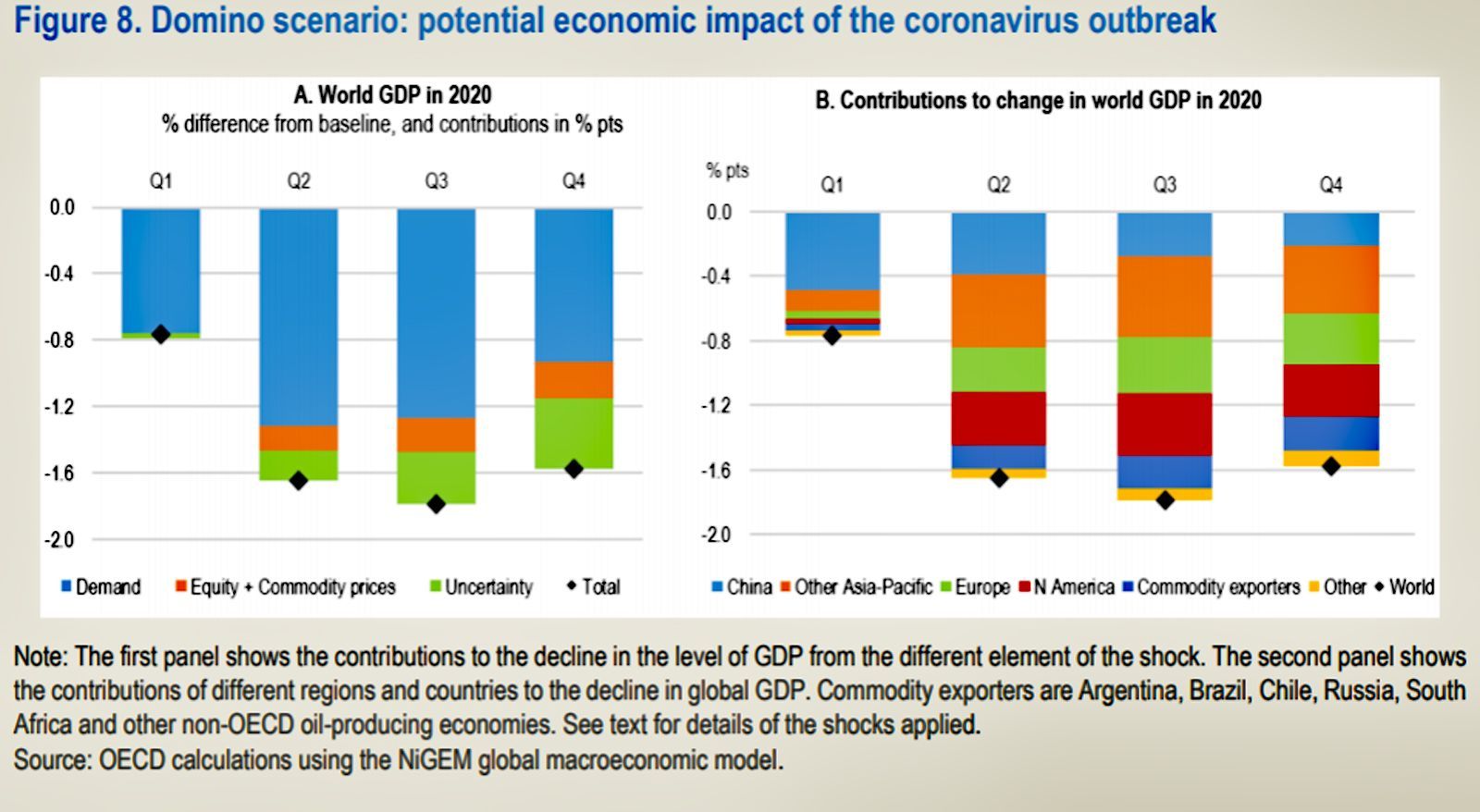

The major part of the decline in GDP again stems from the direct effects of the reduction in demand, but the impact of heightened uncertainty accumulates gradually (Figure 8, Panel A). World trade is substantially weaker, declining by around 3¾ per cent in 2020, hitting exports in all economies.

The deflationary effects of the combined shocks are considerably larger than in the base-case scenario, with consumer price inflation pushed down by around 0.6 percentage point in 2020 in the OECD economies.

Domestic demand in most other Asia-Pacific economies, including Japan and Korea, and private consumption in the advanced northern hemisphere economies is reduced by 2% (relative to baseline) in the second and third quarters of 2020.

Global equity prices and non-food commodity prices are lowered by 20% in the first nine months of 2020. Heighted uncertainty is modelled via an increase of 50 basis points in investment risk premia in all countries in 2020.

Overall, the level of world GDP is reduced by up to 1.75% (relative to baseline) at the peak of the shock in the latter half of 2020, with the full year impact on global GDP growth in 2020 being close to 1.50 %

B) The desired scenario: outbreak spread of COVID-19 contained:

In case the outbreak of the spread of COVID-19 is contained provides a scenario next to an adverse supply-side shock, with an enforced decline in the number of hours worked. However, the effects are mirrored in weaker demand. A decline in confidence, foregone income for laid-off workers, and lower demand for travel and tourism services all hit consumer spending; a eduction in cash-flow and higher uncertainty delay corporate investment; and existing inventory levels are run down due to the disruption of supply chains.

In this contained outbreak scenario domestic demand in China and Hong Kong, China is reduced by 4% in the first quarter of 2020, and 2% in the second quarter of 2020, reflected in both investment spending and private consumption.

Global equity prices and non-food commodity prices are lowered by 10% in the first half of 2020. Higher uncertainty is modelled via a small rise of 10 basis points in investment risk premia in all countries in the first half of 2020. This raises the cost of capital and reduces investment.

All of these shocks are assumed to fade away gradually by early 2021.

Image over the headline.- International Arrivals area at Haneda Airport (Tokyo, Japan). © Haneda Airport

Related external links:

OECD Interim Economic Assessment, 2nd March 2020.- Coronavirus: The World Economy at Risk